The Real Legacy of the ‘Reagan Revolution’

McCain campaign co-chair Phil Gramm is right: We have "become a nation of whiners." But who is whining more than the bankers that former Sen. Gramm's financial deregulation legislation benefited? The very bankers who now expect a government bailout, such as those at UBS Investment Bank, where Gramm found lucrative employment.

McCain campaign co-chair Phil Gramm is right: We have “become a nation of whiners.” But who is whining more than the bankers that former Sen. Gramm’s financial deregulation legislation benefited? The very bankers who now expect a government bailout, such as those at UBS Investment Bank, where Gramm found lucrative employment.

As chair of the powerful Senate Banking Committee, Gramm engineered passage of legislation that effectively ended the major regulatory restraints applied to the financial industry in response to the Great Depression. The purpose of the Gramm-Leach-Bliley Act — co-authored by Gramm, passed in 1999 by a Republican-controlled Congress and signed by President Bill Clinton — was to liberate the banks, stockbrokers and insurance companies from restraints imposed on their activities more than seven decades ago. It was legislation that the financial community, which contributed heavily to Gramm’s campaigns in the previous five years, desperately wanted and obviously has abused. So why now bail these institutions out?

Hows about some “tough love” for those bankers suddenly in trouble? You know, the sink-or-swim approach of “welfare reform” that Gramm and Clinton applied to poor people to end their addiction to government handouts. Or, perhaps a heavy dose of “faith-based” personal responsibility initiatives to get those knaves who messed up our entire housing market back on the straight and narrow. Sounds ridiculous I know, because nothing but the bleeding-heart, big-government, throw-money-at-the-problem approach will do when it comes to salvaging corrupt corporations.

That is the real legacy of what has been ballyhooed as the “Reagan Revolution,” which Clinton went along with, but which found its full flowering in the administration of George W. Bush. The bookends of the Bush years are the Enron debacle and the federal bailout of bankers drunk on their own greed. And no two people in this country are more responsible for enabling this sordid behavior than the power couple Phil and Wendy Gramm.

Enron, lest we forget, was their baby. Then-Sen. Gramm sponsored the Commodity Futures Modernization Act of 2000, which allowed Enron’s scamming to happen. As Ken Lay, who was chair of Gramm’s election finance committee, put it quite candidly when asked for the secret of Enron’s success, “basically, we are entering or in markets that are deregulating or have recently deregulated.”

Part of that deregulation involved rulings of the U.S. Commodity Futures Trading Commission, then chaired by Wendy Gramm, who upon retiring from that post became a highly compensated member of the Enron board of directors, serving for eight years. She even was on the board’s audit committee during the time of the corporation’s despicable financial shenanigans. While on the Enron board, Wendy Gramm also chaired an anti-regulatory think tank that received funding from Enron and other corporations that benefited directly from the policies her institute espoused.

My point here is not to expose the dubious ethics of the Gramms’ various business ventures but rather to question why Sen. John McCain turned to Phil Gramm for leadership in his presidential campaign. Indeed, until his verbal gaffe, Gramm was highly visible and rumored to be the choice for secretary of the treasury should McCain win.

McCain has long promised voters that he learned the hard lessons provided by his being one of the infamous Keating Five in the nefarious savings and loan scandal that cost taxpayers hundreds of billions of dollars. Yet he chose as his campaign co-chair a former senator whose push for government deregulation facilitated the far deeper scandal we now are experiencing. Here is a man whose legislation created what financial guru Warren Buffett termed “financial weapons of mass destruction.”

Why in the world would you designate as your key economic adviser someone who left the Senate to become an officer of the bank that is at the very center of this mess, a former senator who not only secured highly paid employment with a banking giant that benefited from legislation he helped pass, but who then lobbied Congress for even more of the deregulatory breaks that got the bank into such deep trouble?

The answer cannot simply be that McCain doesn’t care much about economics, as he himself has indicated. Perhaps that would explain his having voted for all of the measures pushed through the Senate by Gramm. Perhaps it even would explain McCain’s having been chair of Gramm’s own failed presidential bid. But indifference to economics does not explain the prominence of Gramm in the McCain campaign as the top economic adviser during these past months of the U.S. financial crisis. Indifference to the folks losing their homes is a more plausible explanation.

Robert Scheer is the author, most recently, of “The Pornography of Power: How Defense Hawks Hijacked 9/11 and Weakened America,” published by Twelve Books.

Your support matters…Independent journalism is under threat and overshadowed by heavily funded mainstream media.

You can help level the playing field. Become a member.

Your tax-deductible contribution keeps us digging beneath the headlines to give you thought-provoking, investigative reporting and analysis that unearths what's really happening- without compromise.

Give today to support our courageous, independent journalists.

Editorial Cartoons

Editorial Cartoons

Who would head up such a takeover? The public.

Who would head up such a takeover? The public.

The social media giant's decision to expand its operations in London may hold important clues about the future of the British economy.

The social media giant's decision to expand its operations in London may hold important clues about the future of the British economy.

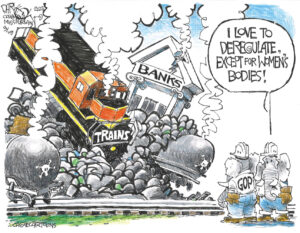

Deregulation is just another form of trickle-down economics in which the gains go to the top and the rest of us bear all the risk.

Deregulation is just another form of trickle-down economics in which the gains go to the top and the rest of us bear all the risk.

On "Late Night with Seth Meyers," the host checks in on the acting Environmental Protection Agency chief, a man Politico recently said "should scare anyone who breathes."

On "Late Night with Seth Meyers," the host checks in on the acting Environmental Protection Agency chief, a man Politico recently said "should scare anyone who breathes."

A fundamental battle for democracy is in progress—a conflict over superdelegates to the Democratic Party's national convention in 2020.

A fundamental battle for democracy is in progress—a conflict over superdelegates to the Democratic Party's national convention in 2020.

You need to be a supporter to comment.

There are currently no responses to this article.

Be the first to respond.