The Root of Madoff’s Evil

Bernard Madoff should be exhibit A in why the dark world of totally unregulated private money managers and hedge funds should be opened to the light of systematic government supervision. Instead, he is being treated as an aberrant menace.

How convenient for the judge and the media to paint Bernard Madoff as Mr. Evil, a uniquely venal blight on an otherwise responsible financial industry in which money is handled honestly and with transparency.

Madoff, sentenced Monday to 150 years in prison for bilking investors of billions, should be exhibit A in why the dark world of totally unregulated private money managers and hedge funds should be opened to the light of systematic government supervision. Instead, he is being treated as an aberrant menace, with the danger removed once the devil incarnate, as his victims describe him, is locked up and the key thrown away.

For goodness’ sake this was not some sort of weird outsider who flipped out, but rather a key developer of the modern system of electronic trading and a founder and chairman of Nasdaq. Madoff often was called upon to help write the rules on financial regulation and therefore became quite expert at subverting them.

As Securities and Exchange Commission Inspector General H. David Kotz testified before Congress, the inspector general’s office is looking into “[t]he extent to which the reputation and status of Bernard Madoff, and the fact that he served on SEC Advisory Committees, participated on securities industry boards and panels, and had social and professional relationships with SEC officials, may have affected commission decisions regarding investigations, examinations and inspections of his firm.”

Those relationships were close (the personal ties included the marriage of one of Madoff’s nieces to an SEC official) and stretched out over the decades during which Madoff was a major player on Wall Street. At the very time back in 1999 when the SEC was being formally warned that a Madoff scam was under way, Madoff was consulting with then-SEC Chairman Arthur Levitt Jr. on regulatory matters. When Levitt retired a year later, Madoff was quoted in the trades as paying tribute to him: “He brought all of us to the negotiating table time and time again, on a whole host of issues, and to a greater extent than any other SEC chairman.”

Levitt wrote in a January 2009 opinion article in The Wall Street Journal, “I knew Bernie Madoff and had no reason to believe he was not a legitimate market maker, nor did anyone at that time know he was acting as an adviser to outside investors.”

Nor was he required to tell anyone. And even if he had been, it’s unlikely that part of Madoff’s business would have been looked into. In the deregulatory mania of the preceding two decades, it had been assumed that such managers did not need regulating, and funding for the SEC kept getting cut. As Levitt noted in the article, it would only get worse:

“Since 2002, the number of investment advisers—such as Madoff Securities—has increased by 50%. Yet enforcement resources have been flat or even reduced. … As a result, only about 10% of investment advisers can expect to be examined every three years, and the goal of inspecting every adviser once every five years—laughably light oversight in its own right—has been abandoned.”

Money for proper oversight was not allocated because the prevailing ideology regarding private investment firms — embraced by President Bill Clinton ever as fervently as President George W. Bush would later — was the gospel of radical financial deregulation, a practice that has landed us in the larger banking mess. As with the trading in unregulated derivatives, all of the operations of private investor groups, such as hedge funds, were thought not to require government supervision because these were conducted by professional financiers dealing with sophisticated investors who knew what they were doing. If the investment went south, it was on their dime and there would be no innocent victims.

As we saw with the collapse of AIG and now Madoff, that notion is false because private investment contracts can involve the resources of charitable organizations and pension funds and can end up costing the homes, savings and jobs of ordinary citizens who have no idea of which end of this arcane stuff is up.

When Levitt worked for Clinton as head of the SEC, he teamed up with Alan Greenspan, Robert Rubin and Lawrence Summers to destroy what remained of financial service industry regulation imposed by President Franklin Roosevelt in response to the Great Depression. In recent years Levitt, alone among that gang of four, has criticized that action and accepted some personal responsibility for the subsequent financial meltdown.

He was right again when he stated in his January article: “The Madoff scandal should be a wake-up call for more consistent, uniform, and rigorous regulation of investment advising … the final prod for a fundamental reform of the financial regulatory structure. … ”

He gets it. Let’s hope that Congress does too and is not fooled by the argument of Wall Street lobbyists that Madoff was a lone rotten apple now safely discarded.

Your support matters…Independent journalism is under threat and overshadowed by heavily funded mainstream media.

You can help level the playing field. Become a member.

Your tax-deductible contribution keeps us digging beneath the headlines to give you thought-provoking, investigative reporting and analysis that unearths what's really happening- without compromise.

Give today to support our courageous, independent journalists.

Editorial Cartoons

Editorial Cartoons

If only investors knew exactly what they were getting into—and what they aren’t going to get out of it.

If only investors knew exactly what they were getting into—and what they aren’t going to get out of it.

Investigative reporter Steve Fishman explains how Bernie Madoff was able to pull off one of the largest financial crimes in U.S. history, and whether regulators have taken steps to ensure Americans won't get conned again.

Investigative reporter Steve Fishman explains how Bernie Madoff was able to pull off one of the largest financial crimes in U.S. history, and whether regulators have taken steps to ensure Americans won't get conned again.

For investors who lost money in Bernie Madoff's infamous Ponzi scheme and are waiting for payback from a firm enlisted by the Department of Justice, the check's (still) in the mail.

For investors who lost money in Bernie Madoff's infamous Ponzi scheme and are waiting for payback from a firm enlisted by the Department of Justice, the check's (still) in the mail.

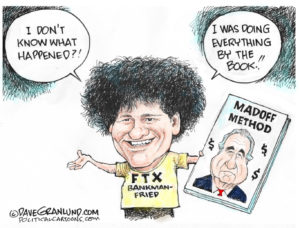

The 32-year-old Turing Pharmaceuticals CEO and Wall Street player became a source of schadenfreude on a mass scale Thursday with the news that he had been arrested for securities fraud.

The 32-year-old Turing Pharmaceuticals CEO and Wall Street player became a source of schadenfreude on a mass scale Thursday with the news that he had been arrested for securities fraud.

Author Gina Nahai's latest novel, "The Luminous Heart of Jonah S.," is a family epic that leaps from Tehran to Los Angeles and back again, blending murder mystery, history, myth and magic in a lively and lyrical read.

Author Gina Nahai knows a thing or two about the Iranian Jewish diaspora in America -- she's part of it.

Author Gina Nahai's latest novel, "The Luminous Heart of Jonah S.," is a family epic that leaps from Tehran to Los Angeles and back again, blending murder mystery, history, myth and magic in a lively and lyrical read.

Author Gina Nahai knows a thing or two about the Iranian Jewish diaspora in America -- she's part of it.

You need to be a supporter to comment.

There are currently no responses to this article.

Be the first to respond.